FINANCE

Remote CFO Services: Transforming Financial Management

In an increasingly digital world, businesses are shifting toward flexible, cost-effective solutions to stay competitive. One of the most impactful changes in financial management is the rise of Remote CFO Services. Companies no longer need to rely solely on in-house executives to manage their finances. Instead, they can access high-level expertise from anywhere in the world. Zari Financials is at the forefront of this transformation, offering professional remote CFO solutions tailored to modern business needs.

What Are Remote CFO Services?

Remote CFO Services provide businesses with access to experienced financial professionals who operate virtually. These experts handle critical financial tasks such as strategic planning, budgeting, forecasting, and financial analysis—without being physically present in the office.

Unlike traditional CFOs, remote CFOs work on a flexible basis, allowing businesses to scale services according to their needs. This approach is particularly beneficial for startups, small businesses, and growing enterprises that require expert guidance but want to avoid the high cost of a full-time executive.

Why Businesses Are Choosing Remote CFO Services

The demand for Remote CFO Services has grown significantly in recent years, and for good reason. Businesses are recognizing the advantages of having a remote financial expert who can deliver results efficiently and cost-effectively.

1. Cost Savings

Hiring a full-time CFO can be a major financial commitment. With Remote CFO Services, businesses only pay for the services they need, making it a budget-friendly option.

2. Access to Top Talent

Location is no longer a barrier. Companies can work with highly skilled CFOs from anywhere, ensuring they get the best expertise available.

3. Flexibility and Scalability

As your business grows, your financial needs evolve. Remote CFO services allow you to scale up or down without the complications of hiring or layoffs.

4. Improved Financial Strategy

A remote CFO brings a fresh perspective and data-driven insights, helping businesses make smarter decisions and achieve long-term growth.

5. Focus on Core Operations

By outsourcing financial leadership, business owners can focus on core operations while leaving complex financial tasks to experts.

Key Services Offered by Zari Financials

At Zari Financials, we provide comprehensive Remote CFO Services designed to meet the unique needs of each client. Our offerings include:

- Strategic financial planning

- Budgeting and forecasting

- Cash flow management

- Financial reporting and analysis

- Risk management and compliance

- Fundraising and investor support

- Performance tracking and KPI development

Our team ensures that your financial systems are not only efficient but also aligned with your business goals.

How Remote CFO Services Drive Business Growth

One of the biggest advantages of Remote CFO Services is their ability to drive sustainable growth. At Zari Financials, we focus on creating strategies that deliver measurable results.

Data-Driven Insights

We analyze your financial data to identify trends, opportunities, and potential risks. This helps you make informed decisions with confidence.

Profitability Optimization

Our experts work to improve your profit margins by identifying inefficiencies and implementing cost-saving strategies.

Cash Flow Stability

Maintaining a healthy cash flow is essential for business success. Remote CFOs ensure your business has the liquidity needed to operate and grow.

Strategic Planning

We help you plan for the future, whether it’s expanding operations, launching new products, or entering new markets.

Who Can Benefit from Remote CFO Services?

Remote CFO Services are ideal for a wide range of businesses, including:

- Startups looking for financial direction

- Small businesses aiming to scale

- Mid-sized companies needing strategic oversight

- Organizations preparing for investment or acquisition

If your business requires expert financial guidance but doesn’t need a full-time CFO, this solution is perfect for you.

Why Choose Zari Financials?

When it comes to Remote CFO Services, choosing the right partner is crucial. Zari Financials stands out for several reasons:

Expertise and Experience

Our team consists of seasoned financial professionals with extensive industry knowledge.

Customized Solutions

We understand that no two businesses are the same. Our services are tailored to meet your specific needs.

Technology-Driven Approach

We use advanced financial tools and software to provide accurate, real-time insights.

Client-Focused Service

At Zari Financials, we prioritize your success. We work closely with you to ensure your financial strategies deliver results.

Signs Your Business Needs Remote CFO Services

Not sure if your business is ready for Remote CFO Services? Here are some common signs:

- You lack clear financial visibility

- Your business is growing rapidly

- Cash flow management is a challenge

- You need help with financial strategy

- You’re preparing for funding or expansion

If you’re experiencing any of these issues, partnering with Zari Financials can provide the clarity and direction you need.

The Future of Financial Management

The future of financial management is digital, flexible, and data-driven. Remote CFO Services are becoming an essential part of modern business strategy, enabling companies to stay agile and competitive. With Zari Financials, you gain access to expert financial leadership that adapts to your business environment. Our remote approach ensures efficiency, transparency, and measurable results.

Conclusion

Remote CFO Services are revolutionizing the way businesses manage their finances. By offering flexibility, cost savings, and access to top-tier expertise, they provide a powerful alternative to traditional financial leadership. Zari Financials is committed to helping businesses succeed through innovative and reliable financial solutions. If you’re ready to take your financial management to the next level, our Remote CFO Services are here to support your journey.

The financial services industry is currently navigating one of its most transformative eras, driven primarily by the rapid evolution of digital infrastructure and shifting borrower expectations. At the heart of this transformation lies origination software, a specialized category of technology that has moved from being a back-office utility to a front-line competitive necessity. For modern banks, credit unions, and independent mortgage lenders, the process of taking a loan from a mere application to a funded account is no longer just a series of administrative tasks; it is a high-stakes digital journey where speed, accuracy, and compliance must coexist perfectly. Origination software acts as the engine for this journey, providing the framework necessary to ingest data, verify identities, assess risk, and ultimately deliver capital into the hands of those who need it.

As we move deeper into 2026, the definition of what constitutes effective origination software has expanded significantly beyond simple data entry forms. Today’s systems are complex ecosystems that leverage artificial intelligence, real-time data integrations, and cloud-based scalability to handle everything from personal micro-loans to multi-million dollar commercial credit facilities. The goal is no longer just to “go paperless,” but to achieve a level of hyper-automation where routine decisions are made in seconds, allowing human underwriters to focus their expertise on the complex, nuanced files that require a personal touch. This article explores the multifaceted world of these systems, detailing how they work, the various forms they take, and why they are indispensable in the current economic environment.

The Core Foundations of Modern Origination Software

Understanding the true value of origination software begins with an appreciation of its core functional architecture. At its most basic level, the software is designed to manage the “front end” of the lending lifecycle, which encompasses the initial point of contact with a borrower and concludes when the loan is either declined or approved and moved into the servicing phase. The beauty of a modern system is its ability to create a seamless flow between these disparate steps, ensuring that no information is lost and no time is wasted in manual handoffs. By centralizing all applicant data, credit reports, and supporting documentation into a single digital “source of truth,” lenders can eliminate the fragmented communication that historically led to long turnaround times and frustrated applicants.

A significant part of this foundational strength comes from the integration of automated decision engines. These engines allow financial institutions to program their specific credit policies directly into the software, ensuring that every application is evaluated against the same rigorous standards without the risk of human bias or error. This level of consistency is not just about efficiency; it is a critical component of regulatory compliance. When an auditor or regulator asks why a certain loan was approved or denied, the origination software provides a clear, timestamped audit trail of every rule that was applied and every piece of data that was considered. In an era where regulatory scrutiny is higher than ever, this transparency is perhaps the most valuable feature a lending platform can offer.

Diverse Categories and Specialized Types

Not all lending is created equal, and consequently, the market for origination software is highly segmented to meet the unique needs of different asset classes. For instance, mortgage origination software is arguably the most complex subtype, as it must navigate a dense forest of federal regulations, property appraisals, and title requirements. These systems are built to handle massive document sets and must interface with external portals for everything from flood insurance verification to secondary market investors. On the other end of the spectrum, we see retail and consumer origination systems, which prioritize speed and a “frictionless” user experience. For a borrower applying for an auto loan or a personal line of credit, the expectation is often an approval within minutes, necessitating a software architecture that can pull credit scores and verify income almost instantaneously.

Commercial lending introduces another layer of complexity that requires specialized origination software. Unlike consumer loans, which are often “scorecard” driven, commercial loans involve the analysis of complex business entities, multiple guarantors, and intricate financial statements. The software used in this space must be able to perform advanced “spreading” of financial data, calculating debt service coverage ratios and other key metrics across various fiscal years. Furthermore, many financial institutions find success by utilizing a modular approach, where they might use a core system for general tasks but integrate specialized “point solutions” for specific niches. This flexibility allows a bank to scale its operations without having to replace its entire technology stack every time it enters a new market or adds a new loan product.

Essential Elements of a High-Performing System

When evaluating what makes an origination software truly world-class, several key elements stand out as non-negotiable in the 2026 landscape. First and foremost is the user interface (UI) and user experience (UX), not just for the internal bank staff, but for the borrower as well. A “borrower portal” that allows customers to upload documents via their smartphones and track their application status in real-time is now a baseline expectation. Internally, the software must be intuitive enough that loan officers can navigate complex files without constant help from the IT department. If the software is too cumbersome, staff will often find manual workarounds, which defeats the entire purpose of investing in automation in the first place.

Another essential element is the depth and breadth of third-party integrations. A standalone origination system is only as good as the data it can access. Modern platforms are built with an “API-first” philosophy, meaning they can easily “talk” to credit bureaus, fraud detection services, employment verification databases, and even alternative data sources like utility payment history or social media signals. This connectivity allows the software to build a 360-degree view of the applicant’s risk profile without requiring the applicant to provide piles of paper documentation. In the center of this technological hub, companies like FICS have established themselves by providing robust solutions that bridge the gap between origination and servicing, ensuring that once a loan is funded, the data flows smoothly into the next phase of the lifecycle without manual re-entry.

The Process of Designing and Implementing a Custom Workflow

Designing the perfect workflow within your origination software is a balancing act between speed and safety. The process typically starts with a thorough “gap analysis” of the institution’s current lending practices to identify bottlenecks where applications tend to stall. Once these areas are identified, the software is configured to automate those specific tasks. For example, if the manual verification of a borrower’s identity typically takes 24 hours, the software can be set up to perform a real-time KYC (Know Your Customer) check against government databases as soon as the application is submitted. This design phase is the ideal time to involve stakeholders from across the organization—from the compliance team to the sales team—to ensure the final workflow meets everyone’s needs.

Implementation is often the most challenging phase of adopting new origination software, as it requires migrating historical data and training staff on the new environment. Successful institutions often take a phased approach, perhaps launching the new software for a single product line like “unsecured personal loans” before rolling it out to more complex areas like “home equity lines of credit.” This allows the IT team to iron out any integration bugs in a controlled environment. Throughout this process, the focus should remain on data integrity. Ensuring that every data point captured during the origination process is “clean” and accurately mapped to the core banking system is vital for long-term reporting and portfolio management.

Analyzing the Costs and Returns on Investment

Investing in top-tier origination software is a significant capital expenditure, but the long-term return on investment (ROI) is often undeniable when calculated correctly. The costs are generally broken down into three buckets: the initial licensing or implementation fees, the ongoing subscription or “per-application” fees, and the internal costs associated with training and maintenance. While the “sticker price” of a premium SaaS (Software as a Service) platform might seem high, it is important to weigh this against the cost of inefficiency. If a manual process costs a bank $500 in labor per loan file, and the software reduces that to $50, the system can pay for itself within a few thousand applications.

Beyond the direct labor savings, origination software provides “soft” ROI in the form of improved conversion rates. In the digital age, borrowers are notoriously impatient; if a bank takes three days to respond to an inquiry while a fintech competitor responds in three minutes, the bank will lose the business regardless of their interest rates. Furthermore, by reducing the “loan-to-loss” ratio through better risk assessment tools, the software directly protects the institution’s bottom line. When you factor in the avoidance of regulatory fines and the ability to scale loan volume without hiring more staff, the financial argument for a modern LOS (Loan Origination System) becomes quite compelling for any growth-oriented lender.

Real-World Examples of Digital Transformation

To see the power of origination software in action, one only needs to look at the rise of “Buy Now, Pay Later” (BNPL) services and digital-only “neobanks.” These companies have built their entire business models around the capabilities of high-speed origination engines. They can process millions of small-dollar loan requests with virtually zero human intervention, using sophisticated algorithms to manage risk in real-time. For more traditional institutions, the transformation is often seen in the mortgage space, where the “time to close” has been a perennial pain point. Some forward-thinking credit unions have used origination software to cut their closing times from 45 days down to less than 20, a shift that drastically improves their standing in a competitive real estate market.

Another practical example is found in the “indirect” lending space, such as auto dealerships. When a customer is sitting in a showroom, the dealer needs to be able to send that customer’s information to multiple lenders and get a firm “yes” or “no” before the customer walks out the door. Origination software that provides a direct portal for these third-party partners allows the lender to “capture the deal” at the point of sale. These real-world applications demonstrate that the software is not just a tool for the credit department, but a vital engine for sales and market share expansion.

Common Mistakes and How to Avoid Them

One of the most frequent mistakes organizations make when adopting origination software is trying to digitize a “broken” manual process. Simply taking a slow, inefficient paper-based workflow and turning it into a slow, inefficient digital workflow will not yield the desired results. Instead, lenders should use the software implementation as an opportunity to “re-engineer” the process from the ground up, questioning why every step exists and whether it can be automated or eliminated. Another common pitfall is over-customization. While it is tempting to build a system that perfectly mimics every unique quirk of your institution, this can lead to a “fragile” system that is difficult to update and maintain.

Lenders also frequently underestimate the importance of “change management” among their staff. If loan officers perceive the new origination software as a threat to their jobs or an unnecessary complication, they may resist using it or find ways to bypass its controls. To avoid this, it is crucial to communicate the benefits clearly: the software isn’t there to replace the human, but to remove the “drudge work” so the human can focus on higher-value activities like relationship building and complex deal structuring. Providing comprehensive training and ensuring that the most influential “super-users” are onboard from day one can make the difference between a successful rollout and an expensive failure.

Future Trends in the Lending Technology Space

Looking toward the future, the trends in origination software are pointing toward even greater levels of intelligence and hyper-personalization. We are seeing the emergence of “generative AI” within these systems, which can assist underwriters by summarizing thousands of pages of financial documents into a concise risk narrative. There is also a growing movement toward “open banking,” where borrowers can grant lenders direct, temporary access to their bank accounts to verify income and spending patterns in real-time. This eliminates the need for “pay stubs” and “bank statements” entirely, making the application process almost entirely invisible to the consumer.

Furthermore, blockchain technology is beginning to find its way into the “documentation” side of origination software, providing an immutable record of property titles and loan contracts. This could potentially revolutionize the secondary mortgage market by making it much easier for investors to “see inside” a pool of loans with 100% confidence in the underlying data. As these technologies mature, the line between “origination” and “servicing” will continue to blur, creating a continuous, lifelong financial relationship between the lender and the borrower. The institutions that thrive will be those that view their origination software not as a static tool, but as a living platform that must constantly evolve to meet the needs of a digital-first world.

Conclusion

In summary, origination software has evolved into the most critical piece of infrastructure for any modern lending operation. It is the catalyst that allows financial institutions to balance the competing demands of lightning-fast speed, bulletproof compliance, and rigorous risk management. By automating the routine, integrating with the global data ecosystem, and providing a superior experience for both staff and borrowers, these systems empower lenders to grow their portfolios without a proportional increase in overhead. As we have explored, the journey to selecting and implementing the right system is complex, but the rewards—in the form of increased profitability and market relevance—are well worth the effort.

Whether you are a small community bank looking to modernize or a global financial powerhouse seeking to streamline complex commercial operations, the message is clear: your origination software is the face of your institution in the digital age. It is the bridge between a borrower’s need and your ability to fulfill it safely and efficiently. By staying informed about the latest trends, avoiding common implementation pitfalls, and choosing a platform that can scale with your ambitions, you can ensure that your lending business remains competitive and resilient for years to come. The future of finance is automated, integrated, and data-driven, and it all starts with the right origination technology.

Fixed Deposits (FDs) are one of the most popular investment options for individuals looking for secure and stable returns in India. An FD is essentially a savings tool offered by banks and non-banking financial institutions (NBFCs) where the investor deposits a lump sum amount for a fixed period and earns interest on it. While understanding the potential returns from an FD, one tool has gained immense popularity among savers and investors: the FD interest calculator.

This article delves into what an FD interest calculator is and how it simplifies investment decisions. It explores its functionality, advantages, and application in financial planning while incorporating examples and calculations in Indian currency.

Understanding the FD Interest Calculator

An FD interest calculator is a digital tool used to estimate the interest income and maturity value of a fixed deposit investment. Available on various websites and mobile applications, including those of banks and other financial institutions, these calculators employ formulas and algorithms to compute results based on input data provided by the investor.

This tool simplifies what can otherwise be a complex calculation, allowing users to quickly understand how much interest they can expect to earn and how their investment will grow over the tenure of the FD.

How Does the FD Interest Calculator Work?

The FD interest calculator uses a mathematical formula to compute the maturity amount and interest earned on your investment. There are two ways the interest on an FD can be calculated:

1. Simple Interest (SI)

SI is typically used for short-term FDs. The formula for simple interest is:

SI = (Principal × Rate × Time) ÷ 100

For example, if you invest ₹50,000 in an FD with an annual interest rate of 6% for 2 years, the simple interest is calculated as follows:

SI = (50,000 × 6 × 2) ÷ 100 = ₹6,000

Here, the maturity amount at the end of 2 years will be:

Principal + SI = ₹50,000 + ₹6,000 = ₹56,000

2. Compound Interest (CI)

Most FDs calculate interest using the compound interest formula. This offers higher returns as the interest earned is reinvested periodically. The formula for compound interest is:

CI = Principal × [(1 + Rate ÷ n) ^ (n × Time)] − Principal

Where:

- Principal: The amount you invest

- Rate: Annual interest rate (expressed in decimals)

- n: The number of times the interest compounds in a year

- Time: Tenure of the FD

To illustrate, let’s say you invest ₹1,00,000 in a fixed deposit with an annual interest rate of 7%, compounding quarterly, for 5 years. The compound interest and maturity value are calculated as:

CI = ₹1,00,000 × [(1 + 0.07 ÷ 4) ^ (4 × 5)] − ₹1,00,000

CI = ₹1,00,000 × (1.0175 ^ 20) − ₹1,00,000

CI = ₹1,00,000 × 1.3728 − ₹1,00,000

CI = ₹37,280 (Interest)

The total maturity amount is:

Principal + CI = ₹1,00,000 + ₹37,280 = ₹1,37,280

The FD interest calculator automates these calculations by requiring users to input the principal amount, tenure, interest rate, and compounding frequency. Based on this data, the tool provides the maturity amount instantly.

Why Use an FD Interest Calculator?

The FD interest calculator offers several benefits that make it an indispensable tool for investors:

1. Time Efficiency

Manual calculations for compound interest can be tedious and prone to errors. Using an online FD interest calculator simplifies this task, providing precise results instantly.

2. Accuracy

By automating calculations, FD interest calculators eliminate errors that can arise from manual computation, ensuring you get accurate predictions.

3. Investment Planning

These tools allow users to compare different investment scenarios. For instance, you can analyze how increasing the principal amount or extending the tenure impacts the returns.

4. User-Friendly

FD interest calculators are available online and are simple to use. You typically need to input the following details:

- Deposit amount (principal)

- Tenure of the FD

- Interest rate

- Compounding frequency (monthly, quarterly, semi-annually, or annually)

In one click, users receive detailed projections, including total interest earned and final maturity value.

Application of FD Interest Calculators in Real-Life Scenarios

FD interest calculators help investors make well-informed decisions based on objective data. Here are some examples:

1. Choosing the Right FD Tenure

For instance, if you wish to invest ₹2,00,000, an FD interest calculator might show the maturity values for different tenure options.

If the annual interest rate is 6.5% compounded quarterly:

- 5 years: ₹2,74,389

- 7 years: ₹3,21,214

Comparing these results, you can decide your tenure based on how much interest you wish to earn.

2. Optimizing Investments Across Banks

Interest rates can vary across banks. By using the calculator, you can evaluate which institution offers the best returns for your investment.

For instance:

- Bank A offers 6% interest compounded annually for 3 years on ₹1,00,000. Maturity value: ₹1,19,101

- Bank B offers 6.2% interest compounded quarterly for 3 years. Maturity value: ₹1,19,967

An FD interest calculator clarifies which bank provides better returns.

3. Tax Planning

Interest earned from FDs is taxable. By using an online FD calculator, you can determine the total interest income and plan your tax liabilities accordingly.

Limitations of FD Interest Calculators

While FD interest calculators are undeniably valuable, they are not without limitations:

- Generalized Calculations: These tools compute maturity amounts based on standard interest rates and do not account for changes in interest rates over the tenure.

- Excludes Taxation: FD interest calculators do not factor in applicable taxes like TDS (Tax Deducted at Source).

- Depends on Accuracy of Inputs: Faulty inputs such as incorrect tenure or interest rate can lead to inaccurate results.

Where to Find FD Interest Calculators?

FD interest calculators are commonly available for use on bank websites, NBFC portals, and financial service provider platforms. Most of these tools are free and accessible online. Simply type “online FD interest calculator” in your search engine, and you’ll have numerous options to choose from.

Conclusion

An FD interest calculator is a vital tool for investors looking to simplify calculations and make informed investment decisions about fixed deposits. By providing immediate and accurate results, it enables users to assess returns, optimize investments, and plan their financial future. Be it for comparing FD schemes offered by different banks or determining the impact of tenure on interest earned, this tool significantly enhances transparency around investment performance.

However, investors must exercise caution and comprehensively evaluate all factors in the financial market, including tax implications, interest rate fluctuations, and institutional credibility, before making final decisions.

Summary

An FD interest calculator is an online tool designed to estimate the interest earnings and maturity amount of your fixed deposit investment. By allowing users to input the deposit amount, tenure, interest rate, and compounding frequency, it provides instant and error-free results. Whether you’re comparing FD schemes or exploring tenure options, this calculator aids in optimizing your financial decisions.

In practical terms, the FD interest calculator eliminates the need for manual calculations and highlights the impact of variables like compounding interest and different interest rates. For example, if you invest ₹1,00,000 at an annual rate of 7% compounded quarterly for five years, you stand to earn a maturity value of ₹1,37,280. Such precision empowers investors to strategize effectively.

Despite its usefulness, the tool has limitations, including non-inclusion of tax deductions and external financial factors. Investors must weigh pros and cons and research thoroughly before finalizing their decisions in the Indian financial market.

Disclaimer:

The content provided is for informational purposes only and should not be considered as financial advice. Investors must analyze all associated risks, tax implications, and other factors before making investment decisions in the Indian financial market.

The manufacturing industry is a cornerstone of global economies, driving innovation, employment, and production. However, it is also notoriously capital-intensive, demanding significant investments in machinery, infrastructure, and technology. Businesses in this sector must carefully evaluate their expenditures to remain competitive and profitable. This is where capital budgeting comes into play—a critical financial tool that helps manufacturing companies assess the viability of business ideas before committing substantial resources. This article explores how capital budgeting helps evaluate manufacturing business ideas and ensures better decision-making for long-term success.

What Is Capital Budgeting?

Capital budgeting is the process of planning, analyzing, and deciding on long-term investments aimed at generating the best possible returns for businesses. This method revolves around determining whether a particular investment or project is worth the allocation of capital. Typically, capital expenditures include purchasing new machinery, building facilities, upgrading technology, and securing patents—especially relevant in the manufacturing sector.

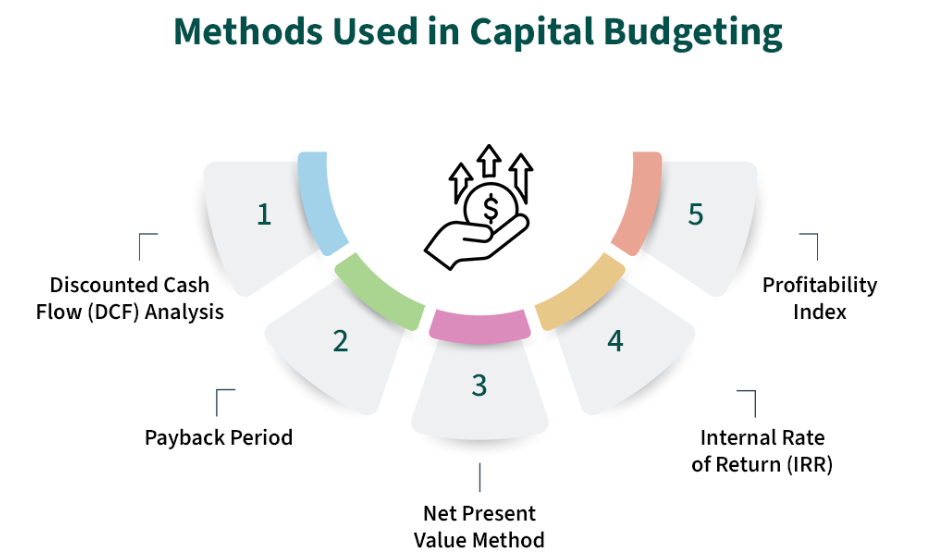

Key Capital Budgeting Techniques

The ultimate goal of capital budgeting is to use limited resources effectively by identifying projects that promise favorable financial outcomes and align with the company’s strategic objectives. The process uses several financial techniques, including:

Net Present Value (NPV)

- Net Present Value (NPV): Calculates the present value of future cash flows from a project, minus the initial investment cost.

Internal Rate of Return (IRR)

- Internal Rate of Return (IRR): Estimates the profitability of potential investments by determining the discount rate at which the net cash flows equal the initial investment.

Payback Period

- Payback Period: Assesses how long it will take for a project to recoup its initial costs.

Profitability Index

- Profitability Index: Measures the ratio between the present value of future cash flows and the initial investment.

Discounted Cash Flow (DCF)

- Discounted Cash Flow (DCF): Evaluates future cash flows by projecting them to their present value.

By relying on quantitative analysis, capital budgeting eliminates guesswork and ensures that manufacturing companies make informed decisions about which business ideas to pursue.

Role of Capital Budgeting in Evaluating Manufacturing Business Ideas

Manufacturing companies often face several challenges when exploring new opportunities, whether launching a new product line, expanding factories, or introducing automated systems. Capital budgeting enables these businesses to methodically assess the viability of various manufacturing business ideas.

Below are several ways capital budgeting benefits the evaluation process:

1. Strategic Alignment

One of the key functions of capital budgeting is to ensure that investments align with the company’s long-term goals and vision. Manufacturing businesses often operate in highly competitive markets, where their strategic focus might vary—from cost leadership to product differentiation.

For example, adopting automation technology might be a strategic decision for a manufacturing firm focused on efficiency. Through capital budgeting, the company can analyze whether such a decision will deliver adequate return on investment (ROI) while remaining consistent with its broader goals, such as reducing production costs or increasing capacity.

By providing measurable data, capital budgeting avoids random decision-making, ensuring that investments driven by boardroom discussions align with measurable success criteria.

2. Financial Viability of Manufacturing Business Ideas

Before plunging millions into capital-intensive projects like new manufacturing lines or state-of-the-art equipment, businesses must ensure the financial viability of their ideas. Manufacturing typically relies on large-scale production, which requires substantial upfront costs. Mistakes in this phase could lead to financial losses that are virtually irrecoverable.

Capital budgeting allows companies to assess financial feasibility, weighing factors such as:

Key Financial Considerations

- Initial Investment Costs: These include purchasing equipment, infrastructure setup, training staff, and other preparation costs.

- Operating Costs: Manufacturing businesses should consider how much additional expense arises from operating the new systems or processes.

- Revenue Projections: It is essential to forecast the revenue that the business idea could generate to determine whether it outweighs the investment.

Using financial techniques such as NPV or IRR, companies can determine whether the cost of the project justifies the returns, thereby mitigating the risk of making poor investment choices.

3. Risk Assessment

The manufacturing industry is fraught with risks, including market fluctuations, unpredictable supply chain disruptions, and regulatory changes. Moreover, investments in capital projects often involve long-term financial commitments, which can make businesses vulnerable if unforeseen circumstances occur.

Capital budgeting plays a vital role in helping manufacturing businesses evaluate the risks associated with their ideas. By analyzing potential cash flows, external market conditions, and project timelines, capital budgeting highlights weaknesses or potential issues in a plan. For example:

Risk Factors Evaluated

- If a manufacturing business idea depends on volatile raw material prices, capital budgeting can help forecast how fluctuations could affect profitability.

- If the proposed project seems overly dependent on untested technology, this approach can scrutinize its reliability by factoring potential risks into financial analysis.

This systematic evaluation ensures that business leaders are fully aware of potential risks before proceeding, and they can even design contingency plans as part of the project approach.

4. Resource Allocation

Efficient management of resources is critical for manufacturing businesses, where capital often competes against competing projects. For instance, a company might be considering implementing a new machinery line while simultaneously evaluating expanding its manufacturing facility. However, it often has a limited budget to allocate.

Capital budgeting serves as a resource allocation tool, enabling decision-makers to prioritize investments more effectively. By comparing and contrasting different initiatives through the application of financial metrics, companies can decide which manufacturing business ideas deserve investment based on their potential profitability, strategic significance, and risks.

This level of financial scrutiny prevents resource mismanagement and ensures that every dollar spent contributes positively to the company’s success.

5. Long-Term Financial Planning

Capital investments typically have long-term ramifications, spanning multiple years—or even decades. As such, manufacturing companies must adopt a forward-looking perspective when evaluating business ideas.

Capital budgeting facilitates long-term financial planning because it considers the full project lifespan, not just immediate impacts. It factors in how investments will play out over the years, examining cash inflows, depreciation, maintenance costs, and probable return rates. For example, companies investing in eco-friendly packaging machinery can use capital budgeting to determine whether the lifetime savings from reduced packaging material outweigh initial investment costs.

This foresight helps businesses avoid being blindsided by future challenges and ensures consistent financial stability.

6. Enhancing Competitive Advantage

Capital budgeting supports manufacturing businesses in achieving competitive advantage by enabling them to explore innovative ideas without risking financial health. Manufacturing industries are constantly innovating, with developments such as Industry 4.0, automation, and lean manufacturing reshaping operations and supply chains.

Manufacturing firms can use capital budgeting to assess whether adopting advanced technologies, such as Artificial Intelligence (AI)-enabled equipment, would enhance their operations and improve market competitiveness. If the analysis reveals that such investments yield better quality products and faster delivery times, this can differentiate them from competitors and strengthen their market position.

Ultimately, strategic investments guided by capital budgeting propel businesses into leadership roles within their industries.

7. Mitigating Bias in Decision-Making

Decision-making in the manufacturing sector can be subject to biases, especially when high-ranking executives or influential stakeholders push for personal preferences rather than relying on objective analysis. This can lead businesses to pursue projects that lack the financial portfolio to succeed.

Capital budgeting removes emotional factors and subjective opinions from investment decisions. By focusing strictly on data, projections, and financial metrics, businesses reduce the likelihood of investing in poorly conceived manufacturing business ideas. For example, capital budgeting could reveal that manufacturing a particular product would result in negligible profits—despite its seeming appeal to executives.

This unbiased approach ensures rational decision-making and helps manufacturing firms avoid costly mistakes driven by internal pressures or groupthink.

8. Sustainability and Environmental Considerations

In recent years, sustainability has become a major focus for manufacturing businesses due to growing environmental regulations and consumer expectations. Adopting environmentally friendly practices or investing in clean energy solutions can be both beneficial and challenging.

Capital budgeting allows manufacturing firms to integrate environmental costs and benefits into their financial evaluations. For instance, investing in energy-efficient machinery might involve high initial costs; however, capital budgeting can project long-term savings from reduced energy consumption, lowered utility bills, and incentives for green practices.

This holistic approach enables businesses to strike the right balance between profitability and environmental responsibility, aligning with modern trends in corporate governance and sustainability.

Key Techniques of Capital Budgeting in Manufacturing

When manufacturing companies evaluate business ideas through capital budgeting, several financial techniques become invaluable. Here is an overview of the most commonly used methods:

Net Present Value (NPV)

Net Present Value assesses profitability by calculating the difference between the present value of cash inflows and the initial costs. In manufacturing, NPV helps businesses determine whether investments in assets like machinery or facilities will yield sufficient future returns.

A positive NPV indicates that the project will generate more income than it costs, making it a worthwhile endeavor. Conversely, a negative NPV suggests the idea is financially unviable.

Internal Rate of Return (IRR)

IRR calculates the discount rate at which the project breaks even. Manufacturing businesses often use IRR to gauge if an investment meets their minimum required return.

Higher IRR values typically indicate better potential returns, helping companies choose the manufacturing business idea with the most attractive rate.

Payback Period

The payback period evaluates how long it takes for the investment to be recouped. This method is particularly relevant for manufacturing firms interested in short-term returns, as it identifies projects with quicker ROI periods.

For example, if the business is looking to recover its investment within 5 years, payback period calculations can rule out ideas with extended timelines.

Discounted Cash Flow (DCF)

The DCF method calculates the present value of future cash flows by applying a discount rate. Manufacturing businesses often rely on DCF to project long-term profitability of investments.

Profitability Index

The profitability index compares the ratio of benefits to costs. Manufacturing companies use this tool to rank competing business ideas, especially under constrained budgets.

Conclusion

Capital budgeting is an indispensable tool for manufacturers seeking to evaluate and pursue new manufacturing business ideas effectively. By enabling strategic alignment, mitigating risks, and fostering financial viability, capital budgeting ensures businesses make informed decisions that yield long-term benefits.

Its systematic approach to resource allocation, sustainability planning, and competitive strategy provides manufacturing firms with the ability to adapt to evolving market demands and industry trends. As the manufacturing sector continues to innovate with technologies like automation and AI, capital budgeting remains integral in balancing risk and return for sustainable growth.

For manufacturing businesses aspiring to lead in their respective niches, capital budgeting is not just a financial process—it is a strategic framework for making better decisions, fostering resilience, and scaling successfully in the competitive landscape.

Square Hang Tags for Branding Excellence

Rectangle Tags for Modern Branding and Packaging Identity

Termite Control Treatment Services in Lahore – Protect Your Property Before It’s Too Late

Reid Health Meta Pixel Class Action Lawsuit: Settlement, Patient Data, and Privacy Implications

Ultimate Guide to TechZone Electronics Financing: Flexible Options for Every Budget

MyZaxbysfeedback Survey – How to Claim Rewards and Enhance Your Zaxby’s Experience

-

HEALTH3 months ago

HEALTH3 months agoReid Health Meta Pixel Class Action Lawsuit: Settlement, Patient Data, and Privacy Implications

-

FINANCE3 months ago

FINANCE3 months agoUltimate Guide to TechZone Electronics Financing: Flexible Options for Every Budget

-

HEALTH3 months ago

HEALTH3 months agoMyZaxbysfeedback Survey – How to Claim Rewards and Enhance Your Zaxby’s Experience

-

HEALTH3 months ago

HEALTH3 months agowww.healthsciencesforum.com: Your Complete Guide to Health Insights, Resources, and Community Support

-

HEALTH3 months ago

HEALTH3 months agoBetanden: Meaning, Origins, Modern Usage, and Everything You Need to Know

-

HEALTH3 months ago

HEALTH3 months agoOneShare Health Review 2026 – Plans, Costs, and Member Benefits

-

HEALTH3 months ago

HEALTH3 months agoPet5ardas com: What It Is, What You Need to Know & Safety Insights

-

HEALTH3 months ago

HEALTH3 months agoWater Flosser QXJ0: Ultimate Guide to Effortless and Effective Oral Care